Menu Website

- Home

- MediaOutReach

- FWD survey: Over 60% of Hong Kong and Macau citizens feel stressed about personal finances

FWD survey: Over 60% of Hong Kong and Macau citizens feel stressed about personal finances

Rabu, 20 Mei 2026 | 20:12

HONG KONG SAR -

Media OutReach Newswire

- 20 May 2026– FWD Hong Kong ("FWD") has released findings of the

latest "Consumer Outlook Survey", revealing a general lack of confidence

among the public regarding their personal financial prospects. 64% of

respondents feel "stressed, worried, or getting by" with their personal

finances. This pressure is compounded by their financial concerns for

the next five to ten years, with 58% most worried about the "rising cost

of everyday living", followed by the "high cost of healthcare" (48%)

and "not saving enough for a comfortable retirement" (47%).

A potential four-year wealth span gap in retirement as savings fall short of actual needs

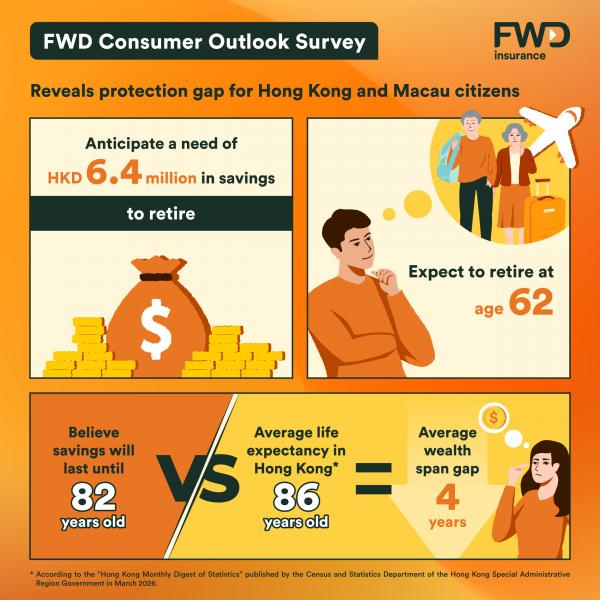

Retirement planning also presents considerable challenges. The survey, which interviewed over 1,000 citizens across Hong Kong and Macau¹, found that respondents expect to retire at an average age of 62, whilst estimating they will require an average of HKD6.4 million in savings to support their retirement years. However, they believe their savings will last for only 20 years, until approximately age 82. Based on the latest Hong Kong government statistics, the average life expectancy in Hong Kong stands at approximately 86 years², which suggests that individuals could face an average wealth span gap of up to four years post-retirement.

Ken Lau, Managing Director, Greater China and Hong Kong Chief Executive Officer, FWD, said: "Hong Kong ranked as the world's longest-living region for ten consecutive years as public health awareness continues to grow3. However, amid rising inflation and escalating healthcare expenses, a potential gap emerges between the public's anticipated retirement savings and their actual savings requirements. This 'longevity risk' must not be overlooked. FWD deeply recognises the challenges and protection needs of individuals throughout different life stages, and we are committed to actively bridging the protection gaps through innovative products and support services. Whether for health protection or wealth management solutions, we are dedicated to being a solid partner for our customers, empowering them to navigate the future with confidence and celebrate living."

Different generations face varied financial challenges: Over 70% of the "Sandwich generation" prioritises family expenses over personal retirement savings; over 60% of respondents aged 45-65 concern savings growth cannot keep pace with rising living cost

The survey found that different generations are grappling with distinct financial concerns:

Clear financial goals but a lack of action – FWD's diversified solutions support the public's overall planning needs

Despite having clear financial planning goals, a significant "say-do gap" in execution is evident. The survey shows that 43% of respondents have not consulted with a financial advisor to review their financial plan, and 30% are not making regular contributions to a retirement fund. Taking the "Sandwich generation" as an example, whilst nearly 40% (39%) express a desire for "a single policy that covers multiple family members", up to 64% lack awareness of such solutions.

Kelvin Yu, Chief Proposition and Healthcare Officer, FWD Hong Kong & Macau, said: "Thanks to ongoing medical technology progress, many diseases treatment options are becoming increasingly sophisticated and personalised, enhancing treatment outcome and patients' quality of life. However, escalating healthcare expenses pose a challenge to individuals' overall financial planning. Therefore, establishing a robust and flexible safety net encompassing both health protection and wealth management is an indispensable component of financial planning across different life stages. FWD continuously drives product innovation, providing solutions such as 'One&All Medical Insurance Plan' which is affordable for all and offering various levels of protection, 'vFamily Medical Plan', and 'MaxFocus Legacy II Insurance Plan' designed for asset growth and legacy planning. Through these diverse and flexible solutions, we continuously support the public's healthcare needs and their overall financial planning."

FWD is committed to addressing the needs of different generations by filling market protection gaps with innovative products

1. The survey was commissioned by FWD and conducted by an independent research agency in the first quarter of 2025, interviewing a total of 1,008 citizens aged 21 to 65 residing in Hong Kong and Macau.

2. According to the "Hong Kong Monthly Digest of Statistics" published by the Census and Statistics Department of the Hong Kong Special Administrative Region Government in March 2026, the provisional figure for the average life expectancy at birth for Hong Kong males in 2025 was 83.3 years, and 88.7 years for females, averaging approximately 86 years.

3. According to the "Hong Kong Monthly Digest of Statistics" published by the Census and Statistics Department of the Hong Kong Special Administrative Region Government in March 2026.

4. The "Family Booster for Parent Option" is an optional benefit available when the policyholder selects Level Connect of the plan. Any benefit amount paid under the Family Booster for Parent Option will not count toward any applicable benefit limits under this plan and will not affect the insured person's eligibility for benefits and/or no-claim premium discounts under this plan.

5. vFamily Medical Plan (Certification Number: F00072) is a Voluntary Health Insurance Scheme plan underwritten by FWD Life Insurance Company (Bermuda) Limited (incorporated in Bermuda with limited liability) (VHIS provider registration number: 00036). The above information is intended to be distributed in the Hong Kong Special Administrative Region only and shall not be construed as an offer to sell, a solicitation to buy or the provision of any insurance products of FWD outside the Hong Kong Special Administrative Region.

6. Family Booster for Child Option is an optional benefit selected by the Policyholder at the time of application for vFamily Medical Plan and is not part of the VHIS certified plan – vFamily Medical Plan (Certification Number: F00072). The benefit amount(s) paid shall not be counted towards any benefit limit(s) as applicable under the terms and benefits of vFamily Medical Plan and shall not affect the coverage available to the insured person of vFamily Medical Plan and/or the eligibility of no claims premium discount of vFamily Medical Plan. The premiums you paid (if any) for the Family Booster for Child Option are not eligible for claiming tax deduction and individual and extra no claims premium discounts available under vFamily Medical Plan. For more details on Family Booster for Child Option, please refer to the product brochure of Family Booster for Child Option (Optional Benefit).

7. In addition to providing coverage for the Insured Person under vFamily Medical Plan, if the Policy Holder applies for Family Booster for Child Option, each of the vFamily Medical Plan's Insured Person's current and/or future children will be entitled to coverage and/or rights under Family Booster for Child Option after the nomination is approved, subject to the corresponding waiting period, benefit limit (if applicable) and terms and conditions.

8. Based on a comparison made by FWD with life insurance plans from major insurance companies in Hong Kong as of 31 October 2025, the expected total return is the fastest in the market. The above example assumes: (i) age next birthday 1, male non-smoker, 2 years premium payment with policy currency of US$, notional amount: US$100,000, annual premium: US$100,000, total premiums paid: US$200,000, (ii) premiums are paid annually and all premiums and applicable insurance levies are paid in full when due, (iii) no cash withdrawal has been made, (iv) no claims have been paid, (v) there is no indebtedness under the policy, (vi) the notional amount of the basic plan remains unchanged throughout the benefit term, (vii) the change of insured option, premium holiday, bonus lock-in option, policy currency conversion option, smart legacy option, policy-split option and incapacity benefit have not been exercised. Past performance is not indicative of future performance.

A potential four-year wealth span gap in retirement as savings fall short of actual needs

Retirement planning also presents considerable challenges. The survey, which interviewed over 1,000 citizens across Hong Kong and Macau¹, found that respondents expect to retire at an average age of 62, whilst estimating they will require an average of HKD6.4 million in savings to support their retirement years. However, they believe their savings will last for only 20 years, until approximately age 82. Based on the latest Hong Kong government statistics, the average life expectancy in Hong Kong stands at approximately 86 years², which suggests that individuals could face an average wealth span gap of up to four years post-retirement.

Ken Lau, Managing Director, Greater China and Hong Kong Chief Executive Officer, FWD, said: "Hong Kong ranked as the world's longest-living region for ten consecutive years as public health awareness continues to grow3. However, amid rising inflation and escalating healthcare expenses, a potential gap emerges between the public's anticipated retirement savings and their actual savings requirements. This 'longevity risk' must not be overlooked. FWD deeply recognises the challenges and protection needs of individuals throughout different life stages, and we are committed to actively bridging the protection gaps through innovative products and support services. Whether for health protection or wealth management solutions, we are dedicated to being a solid partner for our customers, empowering them to navigate the future with confidence and celebrate living."

Different generations face varied financial challenges: Over 70% of the "Sandwich generation" prioritises family expenses over personal retirement savings; over 60% of respondents aged 45-65 concern savings growth cannot keep pace with rising living cost

The survey found that different generations are grappling with distinct financial concerns:

-

- Gen Z (aged 21-29) — The young generation expecting to retire earliest, yet to act on financial planning:

- On average, they expect to retire at 60, the earliest among all generations, and they anticipate needing HKD7.6 million for retirement, also the highest across all generations.

- This high expectation contrasts sharply with their financial planning efforts, where fewer than two in ten(16%) report actively taking concrete steps to safeguard their financial future.

-

- Gen Y (aged 30-44) — The "Sandwich generation" bearing the burden of intergenerational care:

- 57% report that financial support for parents or children accounts for over 20% of their income.

- When faced with additional funds, 71% would prioritise investing in "family's emergency fund", "children's education", or "parents' future healthcare or long-term care", rather than their own retirement savings.

- 29% admit they lack confidence in handling unexpected medical expenses for their family.

-

- Gen X (aged 45-65) — The conservative planners focusing on wealth preservation and inflation-proofing:

- While this generation has started planning for retirement, 62% are concerned that "savings cannot keep up with the rising cost of living", and 36% plan to work part-time or on flexible basis after retirement to supplement their income.

- When choosing retirement solutions, their most desired product features are "guaranteed lifelong income" (58%), followed by "ensuring retirement income grows can keep up with rising costs" (54%), reflecting their emphasis on stable cash flow and wealth preservation.

Clear financial goals but a lack of action – FWD's diversified solutions support the public's overall planning needs

Despite having clear financial planning goals, a significant "say-do gap" in execution is evident. The survey shows that 43% of respondents have not consulted with a financial advisor to review their financial plan, and 30% are not making regular contributions to a retirement fund. Taking the "Sandwich generation" as an example, whilst nearly 40% (39%) express a desire for "a single policy that covers multiple family members", up to 64% lack awareness of such solutions.

Kelvin Yu, Chief Proposition and Healthcare Officer, FWD Hong Kong & Macau, said: "Thanks to ongoing medical technology progress, many diseases treatment options are becoming increasingly sophisticated and personalised, enhancing treatment outcome and patients' quality of life. However, escalating healthcare expenses pose a challenge to individuals' overall financial planning. Therefore, establishing a robust and flexible safety net encompassing both health protection and wealth management is an indispensable component of financial planning across different life stages. FWD continuously drives product innovation, providing solutions such as 'One&All Medical Insurance Plan' which is affordable for all and offering various levels of protection, 'vFamily Medical Plan', and 'MaxFocus Legacy II Insurance Plan' designed for asset growth and legacy planning. Through these diverse and flexible solutions, we continuously support the public's healthcare needs and their overall financial planning."

FWD is committed to addressing the needs of different generations by filling market protection gaps with innovative products

- To address the need of "Sandwich generation" for family medical protection, FWD's "One&All Medical Insurance Plan" allows the insured to add optional benefits4 for their parents who can be covered without health underwriting. Furthermore, FWD's "vFamily Medical Plan" (Certification Number: F00072)5 under the Voluntary Health Insurance Scheme offers the flexibility for the Insured Person to cover multiple children under a single policy with Family Booster for Child Option (Optional Benefit)6, providing coverage to support the healthcare need of a family across two generations7.

- In response to the public's desire for stable wealth growth, FWD's flagship wealth management product, the "MaxFocus Legacy II Insurance Plan", features one of the market's fastest expected total break-even period8 with long-term wealth growth potential to counter inflation challenges, whilst providing customers with greater certainty and flexibility for their legacy planning.

1. The survey was commissioned by FWD and conducted by an independent research agency in the first quarter of 2025, interviewing a total of 1,008 citizens aged 21 to 65 residing in Hong Kong and Macau.

2. According to the "Hong Kong Monthly Digest of Statistics" published by the Census and Statistics Department of the Hong Kong Special Administrative Region Government in March 2026, the provisional figure for the average life expectancy at birth for Hong Kong males in 2025 was 83.3 years, and 88.7 years for females, averaging approximately 86 years.

3. According to the "Hong Kong Monthly Digest of Statistics" published by the Census and Statistics Department of the Hong Kong Special Administrative Region Government in March 2026.

4. The "Family Booster for Parent Option" is an optional benefit available when the policyholder selects Level Connect of the plan. Any benefit amount paid under the Family Booster for Parent Option will not count toward any applicable benefit limits under this plan and will not affect the insured person's eligibility for benefits and/or no-claim premium discounts under this plan.

5. vFamily Medical Plan (Certification Number: F00072) is a Voluntary Health Insurance Scheme plan underwritten by FWD Life Insurance Company (Bermuda) Limited (incorporated in Bermuda with limited liability) (VHIS provider registration number: 00036). The above information is intended to be distributed in the Hong Kong Special Administrative Region only and shall not be construed as an offer to sell, a solicitation to buy or the provision of any insurance products of FWD outside the Hong Kong Special Administrative Region.

6. Family Booster for Child Option is an optional benefit selected by the Policyholder at the time of application for vFamily Medical Plan and is not part of the VHIS certified plan – vFamily Medical Plan (Certification Number: F00072). The benefit amount(s) paid shall not be counted towards any benefit limit(s) as applicable under the terms and benefits of vFamily Medical Plan and shall not affect the coverage available to the insured person of vFamily Medical Plan and/or the eligibility of no claims premium discount of vFamily Medical Plan. The premiums you paid (if any) for the Family Booster for Child Option are not eligible for claiming tax deduction and individual and extra no claims premium discounts available under vFamily Medical Plan. For more details on Family Booster for Child Option, please refer to the product brochure of Family Booster for Child Option (Optional Benefit).

7. In addition to providing coverage for the Insured Person under vFamily Medical Plan, if the Policy Holder applies for Family Booster for Child Option, each of the vFamily Medical Plan's Insured Person's current and/or future children will be entitled to coverage and/or rights under Family Booster for Child Option after the nomination is approved, subject to the corresponding waiting period, benefit limit (if applicable) and terms and conditions.

8. Based on a comparison made by FWD with life insurance plans from major insurance companies in Hong Kong as of 31 October 2025, the expected total return is the fastest in the market. The above example assumes: (i) age next birthday 1, male non-smoker, 2 years premium payment with policy currency of US$, notional amount: US$100,000, annual premium: US$100,000, total premiums paid: US$200,000, (ii) premiums are paid annually and all premiums and applicable insurance levies are paid in full when due, (iii) no cash withdrawal has been made, (iv) no claims have been paid, (v) there is no indebtedness under the policy, (vi) the notional amount of the basic plan remains unchanged throughout the benefit term, (vii) the change of insured option, premium holiday, bonus lock-in option, policy currency conversion option, smart legacy option, policy-split option and incapacity benefit have not been exercised. Past performance is not indicative of future performance.

BERITA LAINNYA

Selasa, 09 Juni 2026 | 22:45

Selasa, 09 Juni 2026 | 22:44

Selasa, 09 Juni 2026 | 22:41

Selasa, 09 Juni 2026 | 22:39

Selasa, 09 Juni 2026 | 22:37

Selasa, 09 Juni 2026 | 22:35

Selasa, 09 Juni 2026 | 22:34

Selasa, 09 Juni 2026 | 22:33

Selasa, 09 Juni 2026 | 22:32

Selasa, 09 Juni 2026 | 22:31

Selasa, 09 Juni 2026 | 22:29

BERIKAN KOMENTAR

-

-

Selasa, 09 Juni 2026 | 23:02

Selasa, 09 Juni 2026 | 23:02

VinRobotics Tandatangani MoU dengan Infineon untuk Kembangkan Robotika Generasi Berikutnya

-

Selasa, 09 Juni 2026 | 23:02

Selasa, 09 Juni 2026 | 23:02

KGI Rilis Outlook Pasar Global Pertengahan Tahun:2026: Secercah Harapan di Tengah Kabut

-

Selasa, 09 Juni 2026 | 23:01

Selasa, 09 Juni 2026 | 23:01

FanRuan Gelar “FANRUAN DATA & AI SUMMIT 2026” di Hong Kong: Data Membentuk AI, AI Mendefinisikan Ulang Keputusan

-

Selasa, 09 Juni 2026 | 23:00

Selasa, 09 Juni 2026 | 23:00

ADHD pada Anak Sekolah di Hong Kong Sering Disalahartikan sebagai “Nakal, Malas, atau Tidak Fokus”

-

Selasa, 09 Juni 2026 | 23:00

Selasa, 09 Juni 2026 | 23:00

Dusit International Perkuat Ekspansi di India dengan Penandatanganan Dusit Princess Rishikesh di Uttarakhand

-

Senin, 08 Juni 2026 | 21:46

Senin, 08 Juni 2026 | 21:46

Muhammad Ramdhani Resmi Dilantik Sebagai Ketua Karang Taruna Kecamatan Dumai Selatan Masa Bakti 2026–2031

-

Sabtu, 06 Juni 2026 | 10:29

Sabtu, 06 Juni 2026 | 10:29

Sun Group debuts at SITF 2026 with exclusive Phu Quoc flight deals and a fresh vision for Vietnam tourism

-

Sabtu, 06 Juni 2026 | 23:42

Sabtu, 06 Juni 2026 | 23:42

Green SM Resmi Luncurkan Green SM Limo di New Delhi, Perluas Layanan Taksi Listrik ke Pasar India

-

Sabtu, 06 Juni 2026 | 23:44

Sabtu, 06 Juni 2026 | 23:44

Belanja Perlengkapan Latihan Andalan Dato' Azizul dengan Pengiriman Super Cepat Shopee

-

Rabu, 03 Juni 2026 | 20:47

Rabu, 03 Juni 2026 | 20:47

Gorilla Technology Group Inc. Announces Pricing of $107 Million Senior Unsecured Convertible Bond Offering

-