Buffalo Potash Announces Preliminary Economic Assessment for Disley Project with After-Tax NPV of US$1.1B and IRR of 30%; Releases Results from Maiden 43-101 Mineral Resource Estimate

Buffalo Potash Announces Preliminary Economic Assessment for Disley Project with After-Tax NPV of US$1.1B and IRR of 30%; Releases Results from Maiden 43-101 Mineral Resource Estimate

Selasa, 28 April 2026 | 07:53

Saskatoon, Saskatchewan -

Newsfile Corp. - April 27, 2026 -

Buffalo Potash Corporation(TSXV: BUFF) (OTCQB: BLPTF) (the "Company" or "Buffalo") is pleased to announce the completion of a Preliminary Economic Assessment ("PEA") and concurrent release of its maiden 43-101 Mineral Resource Estimate for its 100%-owned Disley Potash Project (the "Disley Project"), located in Saskatchewan, Canada.

The PEA has been filed and can be found under the Company's profile on SEDAR+ (www.sedarplus.ca) and on the Company's website (www.buffalopotash.ca).

PEA & Mineral Resource Estimate Highlights

- Total production of 1,000,000 tonnes per annum (TPA) of K62

granular-grade Muriate of Potash (MOP) and 125,000 TPA of K62 soluble

grade MOP

- After-tax NPV(1)(8) of US$1.1B and IRR(1) of 30%

- US$639M initial CAPEX estimate, including US$128M in contingency

- Estimated US$55/t MOP OPEX (Table 4)

- Measured and indicated tonnage of 1,671.5 million metric tonnes at

an average grade of 34.8% KCl, yielding 582 million tonnes of KCl

- Over 50 years of mine life at 1,125,000 TPA based on current resource estimate (Table 2)(2)

- The advancement of a Feasibility Study ("FS") for Disley East and Disley West (the "HLD Mines") will run concurrent with Initial Production Module ("IPM")

construction, with FS completion representing the key decision gate for

proceeding to construction of Disley East and Disley West(3)

(2) Based on Measured and Indicated resource estimate of 582Mt at 34.8% KCl.

(3) The PEA does not constitute a feasibility study and does not demonstrate economic viability

Mr. Steve Halabura P.Geo., Buffalo Chief Executive Officer, commented:

"Since founding Buffalo Potash in 2018, the team and I have invested

years of disciplined work — geological, technical, and strategic — to

systematically unlock the potential of modular selective solution potash

mining in Saskatchewan, the key being Buffalo's Disley Project. Having

spent my career working in Saskatchewan potash, I had a strong

conviction from the beginning that Disley had a substantial resource

endowment, and this Mineral Resource Estimate confirms exactly that. The

PEA illustrates both low capex per tonne and operating cost per tonne,

as well as setting a new environmental standard for how potash

production should look in the 21st century — no tailings stored on surface and minimal freshwater usage."

Mr. Halabura continued: "The team and I believe the Disley

Project represents the next generation of Saskatchewan potash solution

mining and are excited to begin development of the Initial Production

Module, which will be the first leg of this buildout and is expected to

bring soluble-grade potash production online within the next 12 months.

During the development of the Initial Production Module, we will also

test our patent-pending Vortex Crystallizer, alongside an industry

standard crystallizer, which has the potential to significantly reduce

the capex of the Initial Production Module and further potential

build-outs. With global attention turning to the security of critical

supply chains, the urgency to bring reliable, jurisdiction-stable potash

production online has never been greater. This is a proud moment for

our team, our shareholders, and the stakeholders that have supported us

along the way — and we are just getting started."

Table 1: PEA Summary

Line Item

Units

Total Project

Production Rate MOP

TPA

1,000,000

Production Rate Soluble Grade

TPA

125,000

Total Initial CAPEX

US$ million

639

CAPEX per Tonne Capacity

US$/tonne

568

Average Unit OPEX

US$/tonne

55

MOP Price (25-year avg.)

US$/tonne

393.6(4)

Soluble Grade Price (25-year avg.)

US$/tonne

373.6(5)

Pre-Tax NPV(1) (8%)

US$ million

1,534.67

Pre-Tax IRR(1)

%

35

Post-Tax NPV(1) (8%)

US$ million

1,085.47

Post-Tax IRR(1)

%

30

Steady-State Annual Revenue

US$ million

442.5

Steady-State Annual EBITDA

US$ million

251.0

(4) LoM average price of Granular MOP, produced by Disley East and Disley West

(5) LoM average price of Soluble Grade MOP, produced by IPM

The PEA is preliminary in nature and includes inferred mineral

resources, which are considered too speculative geologically to have the

economic considerations applied to them that would enable them to be

categorized as mineral reserves. There is no certainty that the PEA will

be realized.

PEA & Mineral Resource Estimate Overview

The PEA was prepared by Micon International Co Limited ("Micon") in accordance with National Instrument 43-101

Standards of Disclosure for Mineral Projects and evaluates the

development of the Disley Project as a phased potash solution mining

operation. The PEA has an effective date of April 15, 2026 and is based

on a Mineral Resource Estimate ("MRE") developed concurrently by

Micon with an effective date of April 15, 2026, incorporating historical

assay data from legacy drilling programs as well as results from

Buffalo Potash's 2026 confirmation drill program. The PEA contemplates a

phased development approach across three production facilities on the

Disley property:

The Initial Production Module ("IPM") - is a low-capital entry point designed to bring 125,000 tonnes per year of soluble grade MOP to market;

Disley East - a full-scale HLD Mine on the east segment of

the Disley Project, with a production capacity of 500,000 tonnes per

year of granular MOP; and

Disley West - a full-scale HLD Mine on the west segment of

the Disley Project, with a production capacity of 500,000 tonnes per

year of granular MOP.

Successful construction of the IPM is anticipated to provide technical

data used in the completion of the concurrent FS and would, subject to

the results from the FS and a positive construction decision, be

followed by the potential concurrent development of the Disley East and

Disley West HLD solution mines. If fully developed, the Disley Project

is designed to have the capacity to produce 1,000,000 TPA of granular

MOP and 125,000 TPA of soluble grade MOP ("Full Production Capacity").

The MRE indicates a resource base that substantially exceeds the

project's current design requirements, which, if successfully developed,

would position the Disley Project as a long-life asset. This is

consistent with the generational mine lifecycles typically associated

with Saskatchewan potash operations, though there is no certainty that

resources will be converted to reserves or that any particular mine life

will be achieved.

Table 2: Mineral Resource Estimate

Category

Tonnage (Mt)

Avg KCl Grade

Avg K2O Grade

KCl (Mt)

K2O (Mt)

Measured

399.7

34.82%

22.00%

139.2

87.9

Indicated

1,267.4

34.84%

22.01%

441.5

278.9

Inferred

2,663.2

34.96%

22.08%

930.9

588.1

Table 2 Notes:

The effective date of this MRE is April 15, 2026.

Dr. Ryan Langdon, Ph.D, CGeol, of Micon is the QP responsible for this MRE.

The MRE has been classified in the Measured, Indicated and Inferred categories.

An average specific gravity (SG) value of 2.08 g/cm3 was used.

Conversion between KCl and K2O was made using the formula KCl = K2O * 1.583

The MRE used economic assumptions for HLD mining. A deduction was

made to account for the presence of mining anomalies not detected by

existing drill holes and seismic lines. The values used are 5% for

Measured, 9% for Indicated and 25% for Inferred.

The block model supporting the resource is orthogonal and has a block size of 50 m x 50 m x 0.9 m.

The mineral resources described above have been prepared in

accordance with the current Canadian Institute of Mining, Metallurgy and

Petroleum Standards and Practices.

Numbers have been rounded to the nearest million tonnes. Differences may occur in totals due to rounding.

Mineral Resources are not Mineral Reserves as they do not have

demonstrated economic viability. The quantity and grade of reported

Inferred Mineral Resources are uncertain in nature and there has been

insufficient exploration; however, it is reasonably expected that a

significant portion of Inferred Mineral Resources could be upgraded into

Indicated Mineral Resources with further exploration.

Micon's QP has not identified any legal, political, environmental,

or other factors that could materially affect the potential development

of the mineral resource estimate.

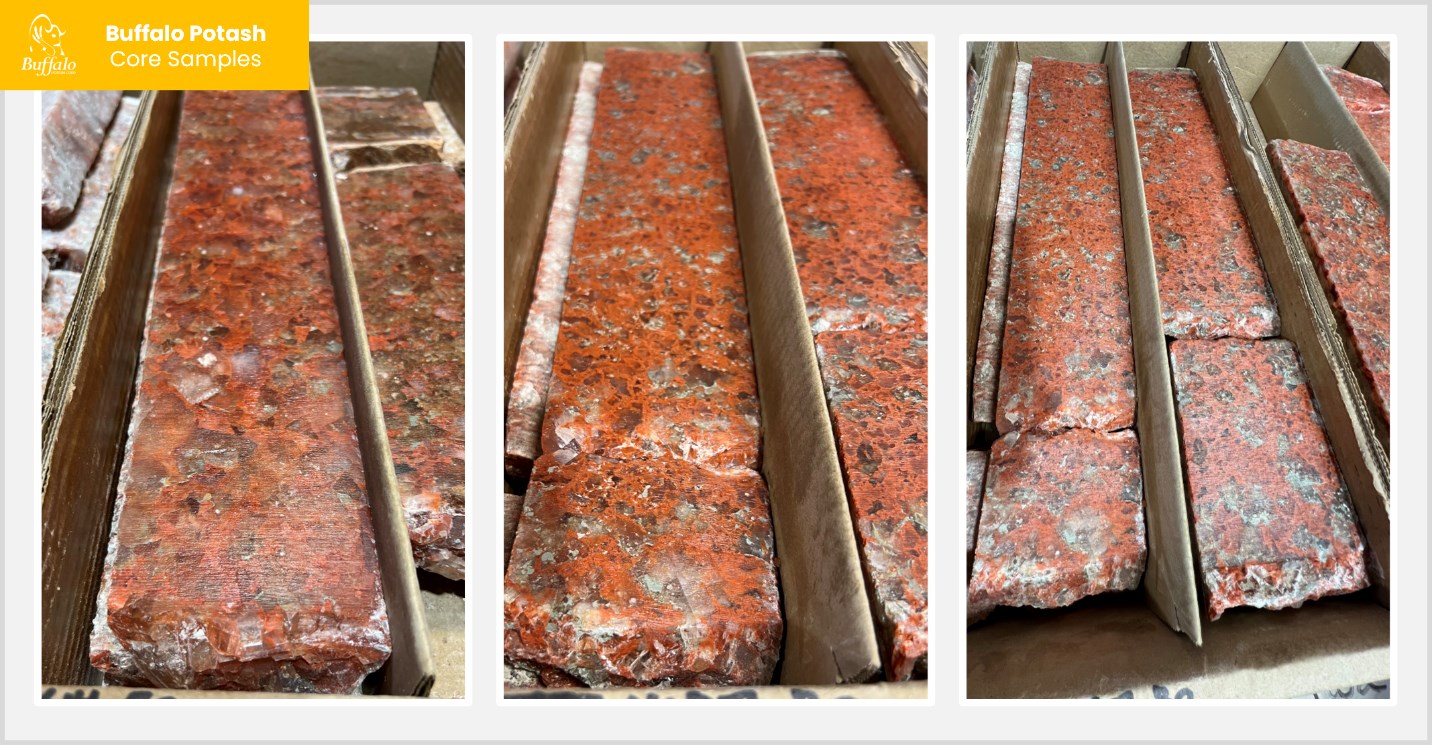

Figure 1: Core Samples from the 7-10 Hole on the Disley Project

Buffalo intends to develop the Project using solution mining, a

well-established approach that has been successfully deployed across

Saskatchewan for more than 50 years. Solution mining is widely

recognized as a reliable and efficient technique for extracting potash

from laterally continuous deposits, notably used at both neighboring

properties of the Disley Project — the K+S Bethune mine and the Mosaic

Belle Plaine mine.

Building on this proven foundation, Buffalo holds a patent on an

enhanced solution mining approach known as Horizontal-Line-Drive

Selective Solution Mining ("HLD Mining"), which is the

installation of commercially proven oil and gas injection systems within

horizontal wells. This method is designed to optimize efficiency,

reduce overall capital intensity, and significantly limit freshwater

requirements, while remaining grounded in the principles of traditional

solution mining.

Following underground dissolution, potash-rich brine is recovered to

surface and processed through crystallization, drying, and compaction to

produce a finished potash product ready for local delivery or export

via existing road and rail infrastructure that currently runs adjacent

to the Disley Property.

Initial Capital Expenditure (CAPEX)

The initial capital cost estimate has been prepared in line with the

Class 4 definition outlined by AACE International standards, with a

contingency of 25% applied to the IPM, Disley East, and Disley West

components.

Mechanical equipment represents the largest component of initial capital

expenditure at approximately 38% of Total Project initial CAPEX. For

Disley East and Disley West, the mechanical scope encompasses the full

processing train required to produce export-grade granular MOP,

including crystallization, debrining and drying, compaction and glazing,

soluble product screening, and product storage and loading. For the

IPM, the mechanical scope includes a crystallizer, pumps, tanks,

pipework, centrifuge, dryer, and baghouse. Total initial capital

expenditure across all three facilities is US$639 million, as summarized

in the table below.

Table 3: Initial CAPEX Summary

Description

IPM

Disley East

Disley West

Total Project

(US$ million)

(US$ million)

(US$ million)

(US$ million)

Site Works

0.7

11.3

11.3

23.3

Concrete

-

5.6

5.6

11.2

Structural Steel

1.2

9.3

9.3

19.9

Mechanical

15.1

113.3

113.3

241.7

Piping

0.2

14.9

14.9

30.0

Electrical

-

15.0

15.0

29.9

Instrumentation

0.1

2.9

2.9

5.9

Architecture

0.0

19.6

19.6

39.2

Minor Mechanical

4.7

2.4

2.4

9.4

General Construction

1.4

13.3

13.3

28.0

Indirects

-

36.1

36.1

72.3

Contingency

5.8

60.9

60.9

127.7

Total Capital Expenditure(6)

29.2

304.7

304.7

638.6

(6) For modelling purposes, the total capital expenditure

estimate for the PEA assumes use of an industry standard crystallizer

instead of Buffalo's patent-pending Vortex Crystallizer.

Sustaining capital of US$483 million (US$17/t MOP) over the life of mine

comprises an annual provision of 2% of original fixed plant and surface

infrastructure costs, plus US$10/t MOP for the drilling, completion and

tie-in of replacement wells — the dominant component of sustaining

capital — based on each set of three wells yielding 500,000 tonnes over

an approximate 5-year useful life.

Operating Expenses (OPEX)

Buffalo Potash's estimated operating cost of US$55/t MOP reflects the

structural advantages of operating in Saskatchewan, a mature potash

jurisdiction with competitive industrial energy rates, an established

skilled workforce, and existing road and rail infrastructure adjacent to

the Disley Property enabling low-cost delivery to both domestic and

export markets. Buffalo management anticipates these fundamentals

position the Disley Project to be among the lowest-cost potash producers

upon reaching full production.

Table 4: OPEX Summary

Item

Description

1,125,000 TPA

(US$ million)

IPM Contingency

$14.49/t applied to IPM production only

1.8

Wellfield Power

500 Hp at $0.063/kWh

1.8

Processing Power

19,356 Hp at $0.063/kWh

18.0

Drilling

$25,000/day; 45 days/yr

0.1

Pipes, Pumps, Valves

Steaming & general maintenance

0.8

Instrumentation

Monitoring & controls

0.4

Labour

32 staff

7.8

Natural Gas

$386/1000m³ incl. carbon tax

19.6

Maintenance

5% of major equipment capital

5.4

Reagents

Dedust oil & anticake amines

2.0

Water

$2.20/m³; 45 m³/hr

1.3

General & Admin Supervision

Management & safety

1.9

Admin Supplies

Office & admin supplies

0.8

Total Annual OPEX

61.7

OPEX US$/t MOP

55 / tonne

Economic Assumptions

The economic analysis evaluates the Disley Project as a phased

development consisting of the IPM to establish early cash flow, followed

by the full-scale HLD Mine comprising Disley West and Disley East. The

IPM was evaluated as a standalone project, with the HLD Mine (Disley

East and Disley West) assessed on an incremental basis and in

combination with the IPM as an overall project. A Discounted Cash Flow

("DCF") model was constructed with the following assumptions:

All costs and revenues are expressed in constant, first quarter 2026

money terms, with no provision for escalation or inflation;

Capital and operating cost estimates denominated in Canadian dollars

have been converted to US dollars at an exchange rate of CAD 1.38 per

USD;

A discount rate of 8% has been applied on an all-equity basis;

The pre-tax results presented include the Saskatchewan Potash

Production Tax (PPT) and royalties but exclude federal and provincial

corporate income tax. The after-tax results include corporate income tax

(Saskatchewan 12%, Federal 15%);

The IPM ramps up over 3 months at 50% of nominal capacity; Disley

West and Disley East have a 6-month ramp-up period at 50% of capacity,

with the Disley East being deferred by a 3-month offset from the West

Section;

It is assumed the IPM is scheduled to begin construction July 2026 with commercial operations starting January 2027;

It is assumed that a positive construction decision will be reached

on Disley West and Disley East. Disley West is scheduled to begin

construction July 2027, with operations beginning July 2029.

Construction at Disley East is scheduled to be the final facility

developed, with construction beginning October 2027 and operations

beginning October 2029;

Soluble grade MOP produced by the IPM is sold locally, incurring a

transport cost of US$10/t compared to US$43/t for export grade granular

MOP railed FOB Vancouver; soluble grade MOP is priced at a US$20/t

discount to granular, reflecting a life-of-mine average of US$373.6/t

versus US$393.6/t FOB Vancouver;

In addition to MOP, the IPM will produce 50,000 m³ per year of KCl

brine that may be attractive to regional oilfield services customers at

an average transport cost of US$10/m³;

Payback period is measured from the start of construction to the point at which cumulative cash flow turns positive; and

Although the project's mine life is anticipated to extend beyond a 25-year time frame, the NPV(1) and IRR(1) calculations reflect a 25-year "LoM" period.

The primary input parameters for the DCF model are outlined in the table below.

Table 5: Summary of Inputs for Economic Analysis

Input Parameters

Unit

Value

Evaluation Base Date - IPM

Date

2026-07-01

Evaluation Base Date - Disley East & Disley West

Date

2027-07-01

Sales: HLD Mine MOP Sales (granular)

TPA

1,000,000

Sales: IPM MOP (soluble)

TPA

125,000

Sales: KCl Brine

m3/yr

50,000

Price: Granular MOP (FOB Vancouver) 25-year average

US$/t

394

Price: Soluble MOP 25-year average

US$/t

374

Price: KCl Brine

US$/m3

43

Transport Costs: Granular MOP

US$/t

43

Transport Costs: Soluble MOP

US$/t

10

Transport Costs: KCl Brine

US$/m3

10

Corporate Tax (Sask. + Canada)

%

27%

Contingency for CAPEX

%

25%

Discount Rate

%

8%

NPV calculation

Years

25

The Disley East and Disley West mines have a start date of construction

later than that of the Initial Production Module, and their IRR(1), NPV(1)

and Payback periods are all calculated from that later date, while the

overall Project results reflect the start date of the IPM. The

individual IPM phase has a payback period of 1.1 years, while Disley

East and Disley West each respectively have payback periods of 2.9

years. The total Project payback of 4.7 years reflects an earlier

calculated start date at the time of first production at the IPM, prior

to first production from Disley East and Disley West.

Table 6: Summary of Outputs

Metric

Unit

Total Project

Initial CAPEX

US$ million

639

OPEX

US$

55 / tonne

Pre-Tax NPV(1) (8)

US$ million

1,534

Pre-Tax IRR(1)

%

35%

Post-Tax NPV(1) (8)

US$ million

1,085

Post-Tax IRR(1)

%

30%

The Disley Project

The Disley Project is located approximately 50km northwest of Regina and

covers 10,610 hectares (Crown and Freehold mineral rights). The

property is situated immediately adjacent to the east of the K+S Bethune

potash solution mine and north of the Mosaic Belle Plaine potash

solution mine — both of which are amongst the largest producing potash

solution mines in the world. In the opinion of management, the Disley

Project is in one of the most favorable areas of Saskatchewan for potash

solution mining (see Figure 2) as evidenced by the success of these

neighboring projects(6).

Figure 2: The Disley Property Situated Amongst Major Potash Solution Mines(7)

Buffalo Potash is an emerging Saskatchewan-based potash developer

pursuing a modular approach to selective solution mining through its

patented Horizontal Line-Drive (HLD) technology. Buffalo is advancing

the Disley Project — located next to several of the most prominent

currently producing potash solution mines in the world — with the

objective of establishing capital-efficient, lower-impact potash

production in one of the world's leading potash jurisdictions.

Qualified Person

The scientific and technical information contained in this news release

has been reviewed and approved by Douglas F. Hambley, PhD, PE, P.Eng.,

PG, an independent consultant of the Company and Qualified Person as

defined under NI 43-101 Guidelines. Dr. Hambley is a globally recognized

expert in potash geology and mine development and has assisted Micon in

their preparation of the MRE and PEA.

All related and pertinent information has also been reviewed for this

news release by Jared Galenzoski, P.Geo, FIMMM as an independent

consultant and Qualified Person as defined under NI 43-101. Mr.

Galenzoski is also an expert in several potash-related fields and has

assisted Micon in their preparation of the MRE and PEA.

Technical Report and Qualified Persons

For more information in respect of the Disley Project, including with

respect to key assumptions, parameters, and methods used to estimate the

MRE, data validation and QA/QC procedures, and the basis,

qualifications and assumptions for the PEA, please refer to the entirety

of the Technical Report prepared by Ryan Langdon, PhD, P.Geol.; Jack

Nagy, PEng; Christopher Jacobs, CEng., MIMMM; and Richard Thompson,

CEng, MiChemE. Each of the aforementioned persons is considered a

"Qualified Person" for the purposes of NI 43-101 and has reviewed and

approved the scientific and technical disclosure contained in this news

release. No limitations were imposed on their verification process.

Readers are cautioned to review the entirety of the PEA as it contains

additional disclosures material to the matters discussed in this press

release.

Notes (7) The K+S Bethune potash solution mine and north of the Mosaic Belle Plaine potash solution mine (together, the "Adjacent Properties")

may each be considered an "adjacent property" (within the meaning of NI

43-101) to the Company's Disley Project. The Company does not have any

interest in either of the Adjacent Properties. The Company believes this

context is useful in illustrating the proven endowment of the district,

while noting that mineralization on adjacent or nearby properties is

not indicative of mineralization on the Company's Disley Project. There

is no guarantee that the Disley Project will yield comparable results to

any of these mines.

Contact

Steve Halabura, P.Geo. | Chief Executive Officer & Director

Email:

steve@buffalopotash.ca | Phone: 1-306-220-7715

(1) Non-GAAP Financial Measures

Net Present Value ("NPV") and internal rate of return ("IRR")

are forward-looking financial measures used by management to evaluate

the economic potential of the Disley Project, as estimated in the PEA.

These measures do not have standardized definitions under IFRS and may

not be comparable to similar measures disclosed by other issuers.

NPV represents the sum of discounted future after-tax cash flows

projected over the 25-year evaluation period at a discount rate of 8%,

net of initial and sustaining capital expenditures. The most comparable

IFRS measure is net income (loss); however, NPV is a forward-looking

measure that reflects projected future cash flows and cannot be directly

reconciled to historical net income. IRR represents the discount rate

at which NPV equals zero across the project's projected cash flows.

These measures should not be construed as alternatives to net income,

comprehensive income, or cash flows from operations as determined in

accordance with IFRS. Readers are cautioned that these measures reflect

PEA-level estimates and are subject to the risks and uncertainties

disclosed under "Forward-Looking Information" below.

Selasa, 28 April 2026 | 09:16

Selasa, 28 April 2026 | 09:16 Selasa, 28 April 2026 | 09:15

Selasa, 28 April 2026 | 09:15 Selasa, 28 April 2026 | 09:13

Selasa, 28 April 2026 | 09:13

Selasa, 28 April 2026 | 09:12

Selasa, 28 April 2026 | 09:12

Jumat, 17 April 2026 | 12:23

Jumat, 17 April 2026 | 12:23

Jumat, 24 April 2026 | 10:16

Jumat, 24 April 2026 | 10:16

{kind=link}

{kind=link}